A car insurance deductible is one of the most important parts of an auto insurance policy, yet it is also one of the most misunderstood. Many drivers focus almost entirely on the monthly premium and overlook the deductible until they file a claim. When that moment arrives, the deductible suddenly becomes very real—and sometimes very expensive.

Understanding how car insurance deductibles work helps you avoid unpleasant surprises, choose a policy that fits your finances, and decide when it actually makes sense to file a claim. In this guide, we explain what a deductible is, when you pay it, how it affects your premium, and how to choose the right deductible based on your situation.

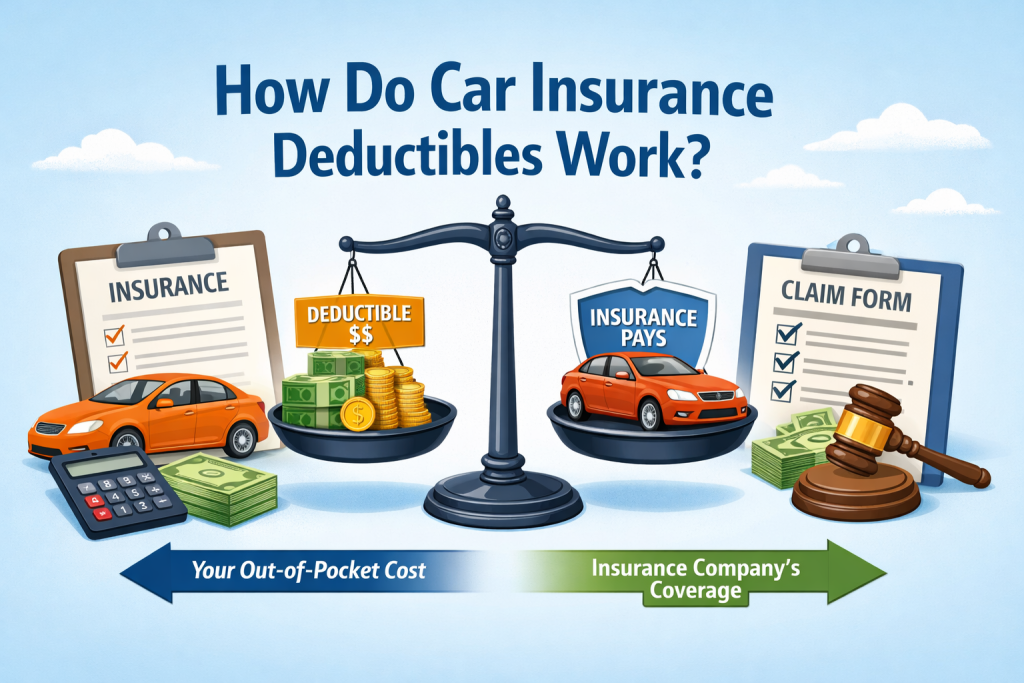

What Is a Car Insurance Deductible?

A deductible is the amount of money you agree to pay out of pocket for a covered claim before your insurance company pays the remaining cost (up to your policy limits). In simple terms, it is your share of the loss.

Deductibles are most commonly associated with collision coverage and comprehensive coverage, which protect your own vehicle. Deductibles are generally not applied to liability coverage because liability pays for damage you cause to others, not damage to your own car.

Example: If your deductible is $500 and a covered repair costs $2,500, you pay $500 and your insurer pays $2,000.

The deductible exists to share risk between you and the insurer. By agreeing to pay part of a loss, you reduce the insurer’s exposure—and that directly affects how much you pay in premiums.

When Do You Pay the Deductible?

You pay the deductible when you file a claim for damage covered by a part of your policy that includes a deductible. This typically happens with collision or comprehensive claims.

There are several common ways deductibles are handled:

- Repair shop payment: the insurer pays the repair shop, and you pay the deductible directly to the shop.

- Reimbursement: you pay the full repair bill and receive reimbursement for the covered amount minus the deductible.

- Total loss settlement: if your car is declared a total loss, the deductible is usually subtracted from the settlement amount.

Key rule: if your policy includes a deductible and you file a covered claim, you are responsible for paying that deductible—regardless of how the claim is paid.

Which Types of Car Insurance Have Deductibles?

Not every part of an auto policy works the same way. Some coverages include deductibles, while others usually do not.

Collision Deductible

The collision deductible applies when you file a claim for crash-related damage to your car, such as hitting another vehicle or an object.

Comprehensive Deductible

The comprehensive deductible applies to non-collision events like theft, vandalism, fire, storm damage, or falling objects.

Liability Coverage (Usually No Deductible)

Liability coverage generally does not include a deductible. Instead of a deductible, liability coverage uses limits that determine the maximum amount the insurer will pay for damage or injuries you cause to others.

Glass and Special Coverages

Some policies treat glass damage differently. Windshield repair or replacement may have a reduced deductible or no deductible at all, depending on policy terms. Always check your policy details rather than assuming.

How Deductibles Affect Your Premium

One of the biggest reasons deductibles matter is their direct impact on your premium.

- Higher deductible = lower premium

- Lower deductible = higher premium

When you choose a higher deductible, you are agreeing to pay more out of pocket if a claim occurs. This reduces the insurer’s risk, which often results in a lower premium.

However, a lower premium is not always the better deal. If a high deductible would be difficult for you to pay on short notice, the savings may not be worth the stress and financial strain.

Real Examples: How Deductibles Work in Practice

Examples make deductibles much easier to understand. Below are common real-world scenarios.

Example 1: Minor Collision

Collision deductible: $1,000

Repair cost: $1,300

You pay: $1,000

Insurance pays: $300

In cases like this, filing a claim may not make sense. The insurer pays very little, and the claim could affect future premiums.

Example 2: Major Collision

Collision deductible: $500

Repair cost: $6,000

You pay: $500

Insurance pays: $5,500

Here, insurance provides significant value. This is exactly the type of loss deductibles are designed for.

Example 3: Comprehensive Claim (Theft)

Comprehensive deductible: $250

Damage from attempted theft: $1,800

You pay: $250

Insurance pays: $1,550

Example 4: Total Loss

If your car is totaled, the insurer pays the vehicle’s covered value (based on policy terms), and the deductible is usually subtracted from that amount.

Do You Pay a Deductible If You’re Not at Fault?

This is a common source of confusion. If you file a claim under your own collision coverage, you may still have to pay your deductible even if the accident was not your fault.

In some cases, your insurer may later recover money from the at-fault party. If that happens, your deductible may be reimbursed. However, reimbursement is not guaranteed and may take time.

Important takeaway: fault does not automatically determine whether you pay a deductible. What matters is which coverage is used to handle the claim.

How to Choose the Right Deductible

Choosing the right deductible is about balancing premium savings with financial comfort.

1) Choose a Deductible You Can Pay Easily

Your deductible should be an amount you can pay on short notice without disrupting your finances. If an unexpected bill would cause stress or debt, the deductible is likely too high.

2) Compare Savings Against Risk

If raising your deductible saves only a small amount per year, it may not be worth the added risk. If the savings are meaningful and you have an emergency fund, a higher deductible can make sense.

3) Consider How You Use Your Car

Drivers who commute daily, drive in heavy traffic, or park in higher-risk areas may face more claim situations. In those cases, a lower deductible can reduce out-of-pocket costs over time.

4) Factor in Vehicle Value

For older vehicles, paying for collision coverage with a low deductible may not be cost-effective. For newer or higher-value vehicles, a deductible you can afford is often more valuable protection.

Common Deductible Mistakes to Avoid

- Choosing the highest deductible just to lower the premium without having savings

- Assuming “full coverage” means no deductible

- Filing small claims close to the deductible amount

- Not realizing collision and comprehensive deductibles can be different

Frequently Asked Questions About Car Insurance Deductibles

Do you pay a deductible for every claim?

Usually yes for collision and comprehensive claims, but not for liability claims.

Can you have different deductibles?

Yes. Many policies have separate deductibles for collision and comprehensive coverage.

Does paying a higher deductible always save money?

Not always. It depends on premium savings, claim frequency, and your ability to pay the deductible when needed.

Conclusion: How Do Car Insurance Deductibles Work?

A car insurance deductible is the amount you pay out of pocket before your insurer covers the rest of a claim. Deductibles play a major role in both your monthly premium and your financial responsibility after an accident.

The right deductible balances affordable premiums with manageable out-of-pocket costs. When you understand how deductibles work in real claims—and choose one you can comfortably afford—you avoid surprises and make your insurance work as a financial safety net rather than a financial shock.